Generally speaking, labour is a businesses biggest expense. Are do you have the right tools, people and processes in place to ensure your teams are operating in the most efficient way possible? Do you or your teams constantly run around burning time chasing information which should be at your fingertips?

Regardless of whether they are documented or not, businesses have well understood process and procedures and they work – but do they work well? The first step is awareness.

This blog will so you how to add another level of analysis to your processes which will provide you with amazing insights and help steer you to continual improvement. It introduces the 4 Processing Detours: Direct, Inconvenient, Supplementary, and Off-Script. It also takes into consideration the unavoidable “forces of nature” to keep our analysis in the real world.

Using examples, it will demonstrate exactly how to examine the real life process Detours – the first step to saving money.

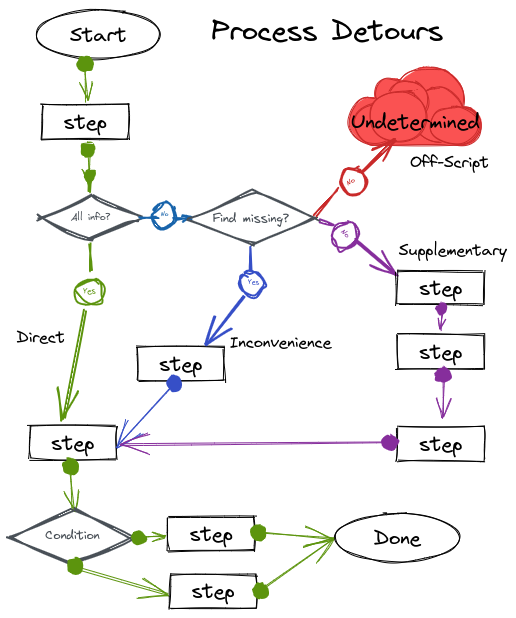

Process Detours

Detours described here are high level and do not describe the intricacies of any individual process. Rather, they are a way of classifying processes based on the ease of execution and whether all the required inputs are present.

A process with all of its inputs available at the time of execution will always perform better then those with missing information. The challenge for the people working those processes is that they are often unaware that inputs are missing until well after commencement.

There are 4 classification of processing Detours:

- Direct

- Inconvenience

- Supplementary

- Off-Script

We will explore each of these shortly.

Time

Before exploring processing Detours, we need to consider how time is related to the execution of a process. Time can be considered in two ways: elapsed time and engaged time.

Elapsed time is the time from begging the process to its completion. Once the clock starts, it does not stop until the process is finished. It ignores whether any activity is being carried out or if the process is sitting idle. It does not take into account how may staff members are contributing when the process is being worked.

Engage time is the total sum of time taken to complete all activities related to the task. Each individual person's time is tallied together to give a final engaged time.

Direct

Direct process follows a well-know well-trodden path to completion and requires no detours from the norm. As with any process, these workflows will branch and can be simple or complex as the specific task necessitates.

For example, an invoice is received from a supplier for goods delivered. On checking the system, the Accounts Payable person will see all goods were received in full and in good condition. The invoice can be processed without delay.

Elapsed time: 5 minutes

Engaged time: 5 minutes

Inconvenience

A inconvenience route in a process is where where a small number of additional steps may be required. This often occurs when some information normally present is missing and person executing the task need to temporarily take a sideways step to find the missing data.

For example, a invoice arrives from a supplier, the Accounts Payable person checks the system to see if the stock has arrived and find that there is no record of the items arriving yet they did see a delivery from that supplier. Unassisted, the Accounts Payable person then diverts to walk over to check the physical paperwork at the warehouse in-tray and found the delivery slip stamped as “Received/Accepted”.

Elapsed time: 10 minutes

Engaged time: 10 minutes

Supplementary

A supplementary route is one where a larger number of additional steps are required and may include additional resources. With each additional step and resource added, time is pulled away form other operations.

For example, a invoice arrives for a supplier, the Accounts Payable person checks the system to see if the stock has arrived and finds that there is no record of the items arriving yet they did see a delivery from that supplier. Unassisted, they then detour to check the physical paperwork at the warehouse in-tray and did not find any delivery slip. They then contact the Warehouse Manager to verify. The Warehouse Manager contacts all warehouse staff. Finally, the Forklift driver then confirms that the goods had been received however the delivery slip was still in his possession.

Elapsed time: 3 hours

Engaged time: Accounts Payable: 15 minutes, Warehouse Manager: 10 min, Forklift driver: 5 min. Total: 30minutes

Off-Script

In these situations, there is no real process to follow.

For example, an invoice arrives from a new supplier for goods commonly use by the business however there is no related purchase order number and no note to say who placed the ordered. The Accounts Payable person cannot determine whether the goods were received. On contacting the supplier, the Accounts Payable person determines that the order was placed over the phone and the sales person from the supplier did not catch the ordering persons name. Given the new relationship, the Accounts Payable person want to keep in good with this new supplier.

Elapsed time: potentially many days

Engaged time: potentially many hours

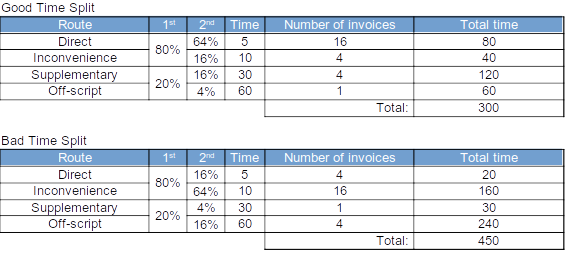

80/20: A law of Nature

Most people are quite familiar with the law of nature also know as the Pareto Principle. For those who don’t know, it basically states that, using sales as an example, 80% of sales come from 20% of the customer. This rule rule of nature and can be applied to just about anything.

Many people accept this rule and leave it there however we can apply this rule to itself giving us more depth of analysis - the 64/16-16/4 rule. 64+16=80, 16+4=20.

What does it all mean?

In an ideal world we would love to totally eliminate Supplementary and Off-script out of our business however nature will not allow that to happen. Therefore, we need to continually refine our processes and push as much as we can towards the Direct route.

To explore what it all means, let’s use and example and assume a few things:

- That the laws of nature (64/16-16/4) are in play and the Accounts Payable person has 25 invoices to process

- Take 80% of invoices and re-apply 80/20

- 64% of 25 = 16 Invoices

- 16% of 25 = 4 Invoices

- Take 20% of invoices and re-apply 80/20

- 16% of 25 = 4 Invoices

- 4% of 25 = 1 Invoice

- Processing times (engaged time) from previous examples will be use.

- That each “Off-script” will take 1 hour.

In the table above, the “Good Time Split” is the desired state. In the real world, we cannot eliminate all exceptions and there will always be times when things don’t go as planned.

In the “Bad Time Split”, we have reversed the balance in the second split. Unfortunately, this second situation occurs quite often and just screams for some process improvement. There is low-hanging fruit here.

Comparing the data between the two tables, it is obvious that there are massive saving by ensuring that at lease 80% of our processes fall into the first 2 processing Detours.

A business with the right information, in the right place, at the right time, this business could be 33% or more better off!